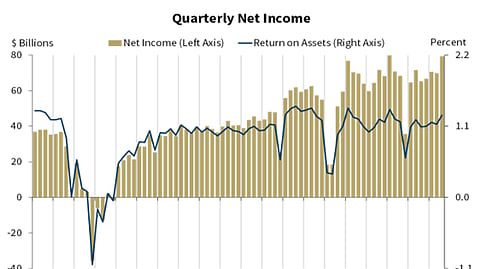

Community bank net income increased 10 percent to $8.4 billion in the third quarter of this year, according to the FDIC third quarter banking profile. .Noninterest income increased 7.1 percent, while noninterest expenses rose 1.7 percent. Nearly two-thirds of community banks saw an increase in net income on a quarterly basis. Community banks’ net interest margin increased for the sixth straight quarter to 3.73 percent, according to the report. Total assets at community banks increased 1.6 percent from the previous quarter and 4.1 percent on an annualized basis to $2.8 trillion. Loan and lease balances at community banks increased 1.3 percent from the second quarter to $1.9 trillion, according to the report. Nearly 70 percent saw growth in total loan balances. “Growth was broad-based across all major portfolios, except auto loans and credit card loans,” according to the report. Community banks’ pretax return on assets increased 13 basis points to 1.46 percent, while net interest income rose 4.1 percent to $958.5 million. Net operating revenue increased nearly 15 percent to $3.8 billion on an annualized basis amid rises in net interest income and noninterest income. The nation’s nearly 4,400 FDIC-insured commercial banks and savings institutions made $79.3 billion in the third quarter, up 13.5 percent or $9.4 billion from the previous quarter. The rise was fueled by increases in net interest income and noninterest income. The banking industry reported $25.1 trillion in total assets in the third quarter, up a half-percent from the previous quarter and 3.7 percent on an annualized basis amid higher total loans and leases, assets in trading accounts and securities. Banks had a 1.27 percent aggregate return on assets, up from 1.13 percent in the second quarter and 1.09 percent in the year-ago quarter. The industry’s NIM increased nine basis points in the third quarter to 3.34 percent, higher than its pre-pandemic average of 3.25 percent, as the yield on earning assets increased 11 basis points, while the cost of funds increased 2 basis points. Net operating revenue increased 3.3 percent or $8.7 billion in the third quarter to $275.1 billion on higher net interest income and noninterest income, according to the FDIC. The efficiency ratio — noninterest expenses as a share of net operating revenue — fell from 55.6 percent in the second quarter to 54.7 percent in the third quarter. Sparked by Fifth Third Bank’s nearly $11 billion acquisition of Comerica, provision expenses fell 30.7 percent to $20.8 billion. The improved NIM “reflects a favorable business environment that allowed banks to lend, support economic activity and maintain financial stability,” said ABA Chief Economist Sayee Srinivasan.Srinivasan said the report “indicates the banking industry delivered a strong third quarter and continued to drive the U.S. economy. Lending grew across most categories for banks of all sizes, deposit growth was healthy and asset quality remained stable.” Other report findings included:Loan and lease balances increased 1.2 percent to $13.2 trillion, with the largest increases in loans to non-depository institutions and loans to acquire or carry securities. Sparked by a rise in uninsured deposits, domestic deposits increased for the fifth straight quarter, this time a half-percent to $92.2 billion amid a rise in interest-bearing accounts. Bank loans 30 or more days past due or in nonaccrual status stayed at 1.49 percent of total loans, which is lower than the pre-pandemic average of 1.94 percent.The number of FDIC-insured institutions fell by 42 to 4,379. Four banks were sold to non-FDIC-insured institutions, while 38 merged with other banks.